GERMANY conceded on Thursday that Greece would need some debt restructuring as part of any new loan programme to make its economy viable as the Greek cabinet raced to finalise reform proposals to avert an imminent economic meltdown.

The admission by German Finance Minister Wolfgang Schaeuble came hours before a midnight deadline for Athens to submit a reform plan meant to convince European partners to give it another loan to save it from a possible exit from the euro.

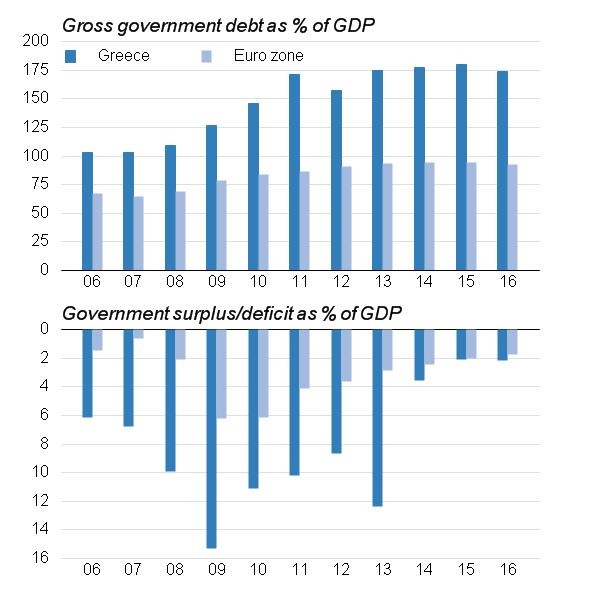

Greece has already had two bailouts worth 240 billion euros from the euro zone and the International Monetary Fund, but its economy has shrunk by a quarter, unemployment is more than 25 percent and one in two young people is out of work.

Schaeuble, who has made no secret of his scepticism about Greece's fitness to remain in the currency area, told a conference in Frankfurt: "Debt sustainability is not feasible without a haircut and I think the IMF is correct in saying that.

But he added: "There cannot be a haircut because it would infringe the system of the European Union."

He offered no solution to the conundrum, which implied that Greece's debt problem might not be soluble within the euro zone.

But he did say there was limited scope for "reprofiling" Greek debt by extending loan maturities, shaving interest rates and lengthening a moratorium on debt service payments.

European Council President Donald Tusk, who will chair an emergency euro zone summit on Sunday to decide Greece's fate, joined growing international calls for Athens to be granted some form of debt relief as part of any new loan deal if Prime Minister Alexis Tsipras finally delivers convincing reforms.

Tsipras chaired a marathon cabinet meeting to finalise a package of tax hikes and pension reforms to send to euro zone authorities in a race to secure agreement at the weekend on a third financial rescue.

The leader of his junior coalition partner, Defence Minister Panos Kammenos, told reporters the Greek proposal had been approved by the cabinet and would be submitted shortly.

Tusk said a realistic proposal from Greece will have to be matched by an equally realistic proposal on debt sustainability from the creditors.

Failure to reach a deal on Sunday, including releasing some money to enable Athens to cover debt service over the next few weeks could lead to a collapse of Greek banks next week.

If there is no agreement, all 28 European Union leaders will discuss measures to limit the damage from a Greek collapse, including humanitarian aid, possible border controls and steps to mitigate the impact on neighbours, EU officials said.

DRAGHI DOUBTFUL

Just how uncertain the coming days are was highlighted when European Central Bank President Mario Draghi voiced highly unusual doubts about the chances of rescuing Greece.

Italian daily Il Sole 24 Ore quoted the ECB chief, under growing fire in Germany for keeping Greek banks afloat, as saying he was not sure a solution would be found for Greece and he did not believe Russia would come to Athens' rescue.

Asked if a deal to save Greece could be wrapped up, Draghi said: "I don't know, this time it's really difficult."

The ECB is keeping shuttered Greek banks afloat with emergency liquidity capped until the weekend.

Even France, Greece's strongest supporter in the euro zone, acknowledged it was working on scenarios for a Greek exit from the currency area if weekend efforts to clinch a deal fail.

Under the agreed timetable, the leftist Greek government, which formally applied on Wednesday for a three-year loan from the European Stability Mechanism bailout fund, has until midnight to present convincing, detailed reform proposals.

FRANKFURT/ATHENS |

VOTE SCENARIOS

What could happen in a YES or NO vote scenario after the July 5th Referendum

THE SOVEREIGN DEBT CRISIS TIMELINE

Greece 10-year government bond yield - percent

GREEK GOVERNMENT DEBT AND DEFICIT

European Commission forecasts through 2016

GREEK GDP PER CAPITA

GDP at market prices per capita rebased to zero at end-2007

GREEK UNEMPLOYMENT RATE BY AGE

Unemployment rate - percent

BANK DEPOSITS

Bank of Greece data to May 2015

SOURCES: GREECE MINISTRY OF INTERIOR, DATASTREAM

by Kathy Lien | BK Asset Management

by Kathy Lien | BK Asset Management

Buy or Sell Euros after Greek Referendum?

Trading tactics become extremely important when it comes to managing positions ahead of major event risks like this weekend's Greek referendum. The referendum may be a yes/no vote on the bailout package but it is also an indirect in/out vote on the euro. Few Greeks truly understand the economic and social consequences of this vote and how more trouble will follow regardless of the outcome. A no vote could lead to a Grexit and a yes vote could mean the resignation of Prime Minister Tsipras along with snap elections. Either way, the one absolute certainty is volatility. When the currency market opened for trading last Sunday, EUR/USD gapped 200 pips lower with similar moves seen in other major currencies. Given the significance of the referendum, we expect the same if not a larger reaction this weekend. U.S. markets are closed on Friday in observation of the July 4th holiday but other markets including currencies are open for trading so the smartest tactic is to go flat ahead of the weekend. Unless you are willing to stomach very wide stops, trading the Greek referendum proactively is extremely dangerous. Even if you handicap the vote correctly, the expected volatility could shake out your trades before it moves in the desired direction. Laying out orders above or below the market is also risky because brokers will fill your trade at unfavorable prices if there is a gap.

However after the referendum, we will be looking to sell euros REGARDLESS of the outcome and here's why.

#1 No Vote - The messiest scenario is if voters reject the referendum. The Greek financial system would collapse and almost immediately investors will question the unity of the euro. Even if a Grexit is long term positive for the monetary union, in the short term, the fear of a Grexit could lead to a multi-day decline in the EUR/USD that takes the currency pair below 1.08. While PM Tsipras will try to use this as leverage to negotiate a new deal with creditors, too many bridges have been burned and in all likelihood there will be no deal and Greece will be pushed out of the euro. In this scenario, we will be looking to sell the EUR/USD on any rally for an eventual target of 1.05.

#2 Yes Vote - A yes vote is just as complicated because it would deepen the political crisis before alleviating the financial one. Tspiras and Varioufakis pledged to resign if voters vote yes which would lead to new elections. Of course given the track record of the Greek government, we would not be surprised if Tsipras decided to remain in office for the sake of executing the people's demands by negotiating a new deal. The question then becomes whether or not Greece and its creditors can agree to a new deal before July 20th, when Greece owes the ECB 3.5 billion euros. A yes vote is encouraging but it does not remove all of the uncertainties and because of that we still think rallies in the EUR/USD should be faded until July 20th. However pricing is key because the EUR/USD will jump on a Yes vote. We will be looking to sell euros between 1.1350 and 1.1550 and not anywhere lower unless the vote is NO.

Dollar - Non Farm Payrolls Take Backseat to Greek Crisis

There was very little consistency in the performance of the U.S. dollar today, which confirms that investors are laser focused on this weekend's Greek crisis. U.S. companies added 223,000 jobs in the month of June, pushing the unemployment rate down to 5.3%. While encouraging this improvement in the jobless rate also reflects a sharp decline in participation. The labor force participation rate fell to 62.6%, the lowest level since 1977 while average hourly earnings growth stagnated. The dollar fell on this report but its losses were limited as investors minimize exposure going into the holiday weekend and the Greek referendum. While Janet Yellen said wage growth is not a prerequisite to near term rate hikes, there's no doubt in our minds that the chance of tightening in September has fallen after today's report. Whether a tightening in the fall is off the table hinges on the Greek crisis and its impact on the global markets. Central banks around the world are getting nervous. This morning the Swedish Central Bank surprised the market with rate cut and more actions could follow in other parts of the world if the Greeks vote NO on Sunday. We are still looking for the dollar to trade as a safe haven currency and a no vote would drive the greenback higher against all of the major currencies except for the Japanese Yen. After today's softer employment report, a rejection of the Greek referendum would be a double blow that could send USD/JPY below 122.

Sterling Hangs Tight Ahead of PMI Services

Amidst mixed economic reports, sterling ended the day unchanged against the U.S. dollar and slightly lower versus the euro. Construction sector activity accelerated in the month of June but house prices fell 0.2% which was a big surprise considering that economists were looking for prices to rise by 0.5%. So far, we've seen weakness in manufacturing and improvements in construction - the deciding factor will be tomorrow service sector report. The uptick in consumer confidence, rebound in retail sales and rise in average weekly earnings means the chance of an upside surprise. Meanwhile the U.K. may come out on top from the Greek crisis. Not only is the country a beneficiary of inflows but British banks have nominal exposure to Greece. According to the Economist, their exposure is worth less than 1% of the value of their equity capital. "British banks' exposures to the likes of Italy, Spain and Portugal amount to 60% of their equity capital. But, unlike when Greece was last under threat in 2012, contagion seems improbable. Indeed, stronger growth in Europe has been contributing to an increase in financial stability, says the report. Without contagion, that should continue." With this in mind, risk aversion could still drive the FTSE lower and lead to near term losses for U.K. assets.

AUD and NZD Hit Hard by Chinese Weakness

The Australian and New Zealand dollars extended their losses versus the greenback today. For the fourth consecutive day, NZD/USD has made fresh 4.5 year lows. While risk aversion dominated the moves, there was no help from economic data. Australia's trade deficit narrowed but not as much as economists had anticipated while commodity prices in New Zealand continued to fall. The persistent weakness of NZD/USD reflects the market's expectations for a rate cut this month. PMI services and retail sales are scheduled for release from Australia. Given the drop in the PMI manufacturing index, we are looking for a downward surprise that could accelerate the losses in AUD/USD. China's HSBC Composite and Services PMI indices are also scheduled for release. While these reports are interesting, the focus is on Chinese stocks. If the Shanghai Composite continues to fall, AUD and NZD will come under additional selling pressure. USD/CAD on the other hand retraced as oil prices recovered.

What happens once a country leaves the euro?

On financial markets a new currency first needs a new currency code that can be identified by computers for trading and payments. They are issued by the Swiss-based International Standards Organisation, a worldwide federation of national standards. It provides an alphabetic three-character code, with the first two letters representing the country and the third the name of the currency. In Greece’s case it could not go back to its old code for drachma, GRD, because there are still some outstanding payments to be made. It would require a new code, most likely GRN.

Is that really all it takes for markets?After that, the code must be entered into software and payments systems so the computers can recognise it for payments processing and trade confirmations and other critical but unseen functions. Market infrastructure providers say this can be done in one business day if needed.

In reality it requires far more. Switching over to a new currency is trickier when it comes to resolving long-dated forward financial contracts, such as swaps and options.

There is a host of legal questions that have to be resolved as payments are switched from one currency to another. Some trades may have to be modified or even rebooked. It is far from an impossible job, but as it involves legal changes, it is a slow and careful process.

Thankfully there is no wall of long-term Greek derivatives trades. The five-year saga has made investors wary and few have accepted Greek central bank-backed collateral for their trades, even if the European Central Bank has permitted it to be used as collateral in Eurosystem monetary policy operations. Some market participants have suggested it could be done in 30 business days but that might prove to be optimistic too.

What would the market expect the Greek government to do to support its new currency?

The Greek government would be likely to set a new Greek currency at half the value of the euro to gain some degree of competitiveness, and enforce that through a mixture of capital controls and currency intervention, and create liquidity through bond issuances.

But how to redenominate euro notes is the hard part. Greece would suffer from disruption to the banking system, bankruptcies, people trying to take their money out of the country illegally and uncertainty about commercial transactions.

It took the euro three years to get from launch date to notes issuance, and although it is unlikely that it would this long for Greece to set up a new currency the process could still take months.

What impact would Greek exit have immediately on the markets?

Market turmoil following an announcement of capital controls or an exit from the euro would not worry a forex settlement service such as CLS.

It is unlikely that there would be a lot of trading business at first though. It is an open question as to how much of the new currency people would have to trade.

Beyond that, Greece would also have to develop a system to settle payments in central bank money, but that could take several years.

Could be a good outcome for Greece?

“Introducing a new Greek currency is do-able over time,” says David Puth, CLS chief executive, “but it is not cost-free.”

“The introduction of a new currency is complex when done in a planned way. When done suddenly and under duress, the process will be disruptive with many unintended consequences that cannot all be anticipated.”

OK, so that’s the Greek side of the saga. What about the euro, is that unaffected?

Not exactly. That is because a Greek exit blows apart the principle sacrosanct to the EU — that eurozone membership is a club you can join but cannot leave. That affects investors, corporations and others with uneven exposure to a break-up of the eurozone.

Such as who?

Such as an Italian manufacturer, say, whose assets and revenues are in Italy but whose financing is done in euros.

So what could it do to protect itself?

James Wood-Collins, chief executive of Record Currency Management, which advises clients on hedging forex exposures, suggests establishing re-denomination swaps or legal tender contracts. They would put a price on the likelihood and impact of a country leaving the eurozone and re-establishing its domestic currency.

“Banks and other market participants have discussed such instruments in recent years, but a market has not yet been established,” he says. “The potential exit of Greece could provide the necessary catalyst for this development.”

(caption by MoneyWeek)

Forex trading, sebagaimana yang kita sedia maklumi, adalah sebuah 'peperangan' harga di antara satu matawang dengan satu matawang yang lain. Lebih tepat lagi ialah peperangan 'nilai' yang seterusnya akan mewujudkan nisbah di antara pasangan matawang.

Apa yang dicari oleh pasangan matawang itu?

Jawapannya ialah KESEIMBANGAN.

Suatu nilai SEIMBANG yang dipersetujui oleh 'sellers' dan 'buyers'.

Ertinya, pasaran akan sentiasa bergerak untuk mencari zon SEIMBANG yang dipersetujui oleh majoriti pelabur, peniaga ataupun peserta pasaran.

Zon Seimbang ini pula sentiasa bergerak dari satu paras ke satu paras yang lain. Makanya, pasaran akan sentiasa berubah-ubah dari suatu Zon Seimbang ke suatu Zon Seimbang yang baru. Keseimbangan ini ditentukan oleh berbagai-bagai faktor, terutamanya sentimen, perspektif mahupun psikologi peserta pasaran. Banyak faktor lain yang turut juga terlibat, antaranya teknikal pasaran itu sendiri.

Makanya, satu pasangan matawang tadi akan sentiasa cuba berada di dalam Zon Seimbang. Sekiranya terdapat faktor-faktor makro mahupun mikro yang signifikan untuk berubah, maka nisbah nilai (yang biasanya kita sebut HARGA) pasangan matawang tadi akan cuba bergerak mencari Zon Seimbang yang baru bagi memenuhi impak faktor-faktor tadi.

Jadi ringkasnya, pasangan matawang itu akan sentiasa berada di:

DALAM ZON SEIMBANG --> LUAR ZON SEIMBANG --> DALAM ZON SEIMBANG BARU

Ada ketikanya, apabila nisbah nilai ('harga') bagi pasangan matawang itu cuba bergerak mencari Zon Seimbang yang baru, nisbah nilai yang baru itu tidak diterima (rejected). Maka nisbah nilai ('harga') akan kembali ke Zon Seimbang yang lama.

Demikianlah kitaran tanpa henti 'peperangan' tadi.

Jadi apa pentingnya kefahaman ini kepada kita para traders?

Jawapannya...

Ya, kita kena TUNGGU... TUNGGU... dan TUNGGU...

Kita perlu mahir untuk mengenalpasti Zon-zon ini supaya dengan itu kita insyaALLAH mampu mengenalpasti PELUANG untuk Entry (juga Exit).

Memanglah penantian itu suatu penyiksaan...

Sebab itu lah posting ini muncul :)

Sebab dah penat tunggu sejak awal pagi, market masih belum SETTLED.

Market belum decide samada nak ke atas atau ke bawah.

Anyway, that's the beauty of it...

Sebab itu, traders yang berjaya adalah traders yang sentiasa punyai tahap KESABARAN yang tinggi!

InsyaALLAH.

Dan yang indahnya pula...

Sabar itu sebahagian dari keimanan... Pesan Rasullullah SAW.

Alhamdulillah...

Salam trading,

Nelayan

FOREX MARKET

Word’s best inside FX traders

The Australian financial regulator ASIC launched an investigation into the 'suspicious trading' responsible for the jump in the AUDUSD just prior to the release of the Reserve bank of Australia surprise decision to hold interest rates in March 3. On April 7 the Reserve Bank of Australia again surprised the market by holding rates. In the minute prior to the report release the market also reacted strongly. The financial regulator ASIC suggested this was evidence of inside trading. But is it really?

Closer examination of the charts casts a better light on this so-called inside trading activity.

The pair in focus is the AUDUSD. Here's the chart for March 3. Quite clearly there is a sharp move before the release of the report. The release time is shown as 13.00 on the 2 minute chart because we use local time on our computer system.

Ok, the major pairs often move together but note the move is not exactly the same as the AUDUSD pair. What happens with the smaller crosses? These CAD and HKD pairs show similar reactions, although the correction following the release is much greater than in the previous charts. Also there is more volume increase in the AUDCAD pair than the AUDHKD pair in the lead-up to the report release.

By now it's going to come as no surprise when the minor currencies like the AUDSGD cross behave in much the same way. However the doji candle pattern with AUDNZD is quite different from the AUDUSD pair and this shows the charts are created in response to completed trades.

Compare the March 3 charts to the release of Australian Reserve bank reports on April 7. The one minute charts from Oanda use our local time, so the official release of the Reserve bank decision is at 14:00. On every one minute chart the market moves dramatically at 13.59 in the minute before the official release of the decision.

AUDUSD

The Oanda 5 second chart for AUDUSD shows the move started at 13:59:50. The move is duplicated on all AUD pairs. By 14:00 all that was left was for the market to digest what had already happened and price activity moved sideways.

The same pattern is repeated on the 5 second chart for the AUDJPY, AUDCAD and AUDSGD pairs.

EUR/AUD

The EURAUD 5 second chart shows exactly the same pattern. The pattern is repeated on the GBPAUD chart

For inside trading to be present we would have to see a significant move in one or two crosses prior to 14:00 AND prior to the broad market move at 13:59. This does not happen.

Australia must have the world's best FX inside traders to be able to take such large positions in every AUD pair at exactly the same time! We take our hats are off to these traders because they have achieved the impossible.

Of course that explanation is plain garbage. A single inside trader might trade one pair, but it is highly unlikely they would have the inclination or the resources to trade EVERY AUD pair.

The exact replication of the fast up move in all AUD pairs in the 2 minutes or 10 seconds prior to the official release of the information is not best explained by inside trading. It is more reasonably explained by the early loading of Reserve Bank information to servers prior to the official release of the data. This is a global market reacting instantly to information as it becomes available to ALL PARTICIPANTS.

The charts clearly show that the Reserve bank information became available to many participants in the minute prior to the official release time. These moves are captured across all pairs by High Frequency Quantitative Trading Algorithms. They have algorithms running in the Dark Pools. These are on the institutional side, not the mums and dads.

The charts clearly suggest that the problem is in the way the Reserve bank loads this data to the web in preparation for its official release. The duplication of behaviour across all AUD pairs shows this information is available to many, if not all, participants at the same time. It's time to call of the FX witch hunt.

The FX market is the deepest and most liquid market in the world. It is arguably the most closely watched and monitored. This intense scrutiny makes it difficult to conduct inside trading. The real concern in the markets associated with the FX market is the manipulation of benchmark interest rates. That task is best left to the banks and other institutions who manipulated LIBOR interest rates and other benchmarks in 2008 and onwards.

Dary Guppy

Founder and Director

Guppytraders.com

Founder and Director

Guppytraders.com

is a beautiful Beaux-arts building in midtown Manhattan. First...</span>")